Of the 66,662 cases reported to the Commission in fiscal year 2025, 324 involved tax fraud. Tax fraud offenses have decreased 12% since fiscal year 2021.1

Click the cover for the PDF handout or learn more below.

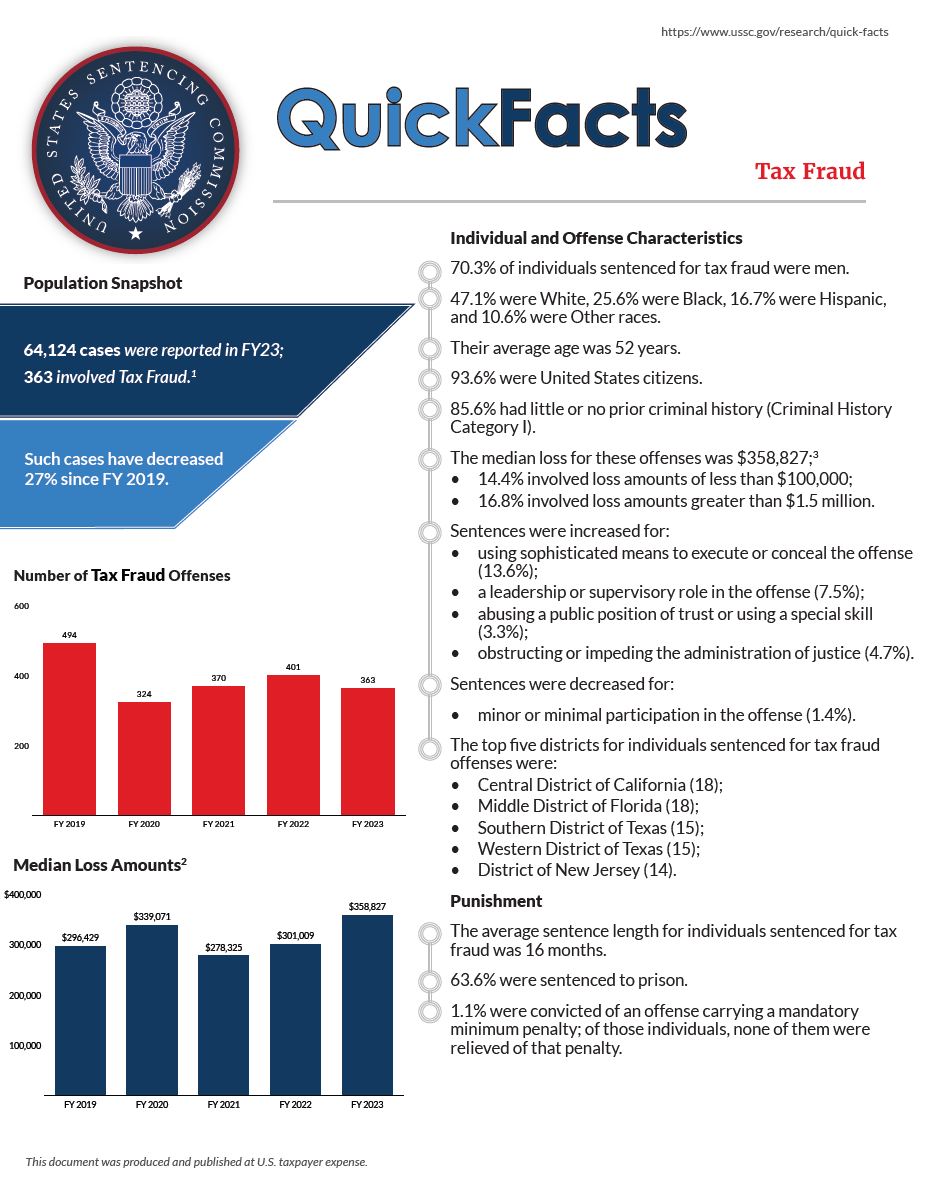

Individual and Offense Characteristics

- 73% of individuals sentenced for tax fraud were men.2

- 51% were White, 19% were Black, 18% were Hispanic, and 12% were Other races.

- Their average age was 53 years.

- 94% were United States citizens.

- 86% had little or no prior criminal history (Criminal History Category I).

- 72% received the adjustment at USSG §4C1.1 for zero criminal history points.

- The median loss for these offenses was $546,562;3

- 7% involved loss amounts of less than $100,000;

- 28% involved loss amounts greater than $1.5 million.

- Sentences were increased for:

- using sophisticated means to execute or conceal the offense (16%);

- a leadership or supervisory role in the offense (6%);

- abusing a public position of trust or using a special skill (2%);

- obstructing or impeding the administration of justice (4%).

- Sentences were decreased for:

- minor or minimal participation in the offense (2%).

- minor or minimal participation in the offense (2%).

- The top five districts for tax fraud offenses were:

- Middle District of Florida (30);

- District of New Jersey (24);

- Southern District of New York (17);

- Central District of California (15);

- Southern District of Florida (14).

Punishment

- The average sentence length for individuals sentenced for tax fraud was 17 months.

- 68% were sentenced to prison.

- No individuals were convicted of an offense carrying a mandatory minimum penalty.

Sentences Relative to the Guideline Range

- 43% of sentences for tax fraud were under the Guidelines Manual.

- 25% were within the guideline range.

- 15% were substantial assistance departures.

- The average sentence reduction was 78%.

- The average sentence reduction was 78%.

- 2% were some other downward departure.

- The average sentence reduction was 60%.

- The average sentence reduction was 60%.

- 25% were within the guideline range.

- 57% of sentences for tax fraud were variances.

- 56% were downward variances.

- The average sentence reduction was 61%.

- The average sentence reduction was 61%.

- 1% were upward variances.

- The average sentence increase was 36%.

- 56% were downward variances.

- The average guideline minimum increased and average sentence imposed have remained steady over the past five years.

- The average guideline minimum was 25 months in fiscal year 2021 and 26 months in fiscal year 2025.

- The average sentence imposed was 14 months in fiscal year 2021 and 17 months in fiscal year 2025.

- The average guideline minimum was 25 months in fiscal year 2021 and 26 months in fiscal year 2025.

1 Tax fraud offenses include cases in which the individual was sentenced under §2T1.1 or §2T1.4 (Tax Evasion; Willful Failure to File Return, Supply Information, or Pay Tax; Fraudulent or False Returns, Statements, or Other Documents or Aiding, Assisting, Procuring, Counseling, or Advising Tax Fraud).

2 Cases with incomplete sentencing information were excluded from the analysis.

3 The Loss Table was amended effective November 1, 2001 and November 1, 2015.

4 “Early Disposition Program” (or EDP) departures are departures where the government

sought a sentence below the guideline range because the defendant participated in the

government’s Early Disposition Program, through which cases are resolved in an expedited

manner. See USSG §5K3.1.

SOURCE: United States Sentencing Commission, FY 2021 through FY 2025 Datafiles, USSCFY21-USSCFY25.